Benefits of an FHA Construction Loan

Low Down Payment: Requires as little as 3.5% of the total project cost.

Flexible Credit Requirements: Accessible to borrowers with lower credit scores.

Single Loan for Construction and Permanent Financing: Simplifies the process and reduces closing costs.

Government Backing: Offers favorable terms like lower interest rates and longer repayment periods.

Customizable Homes: Finance the construction of a custom home tailored to your needs.

Interest-Only Payments During Construction: Eases financial pressure until the home is completed.

Fixed or Adjustable Rates: Choose between fixed and adjustable interest rate options.

Support for Renovations: Can also be used for substantial home improvements.

These benefits make FHA construction loans an attractive option for building a new home or undertaking significant renovations with affordable and flexible financing.

Build Your Dream Home with FHA Construction Loans

Affordable, flexible financing for new constructions and major renovations.

Preparing for an FHA Loan

To qualify for FHA loans, including construction loans, follow these steps:

Maintain Good Credit: Avoid late or missed payments in the 12 months leading up to your application.

Reduce Debt: Work on lowering your debt-to-income ratio.

Avoid New Credit Lines: Do not apply for new credit before or during the loan application process.

Monitor Your Credit Report: Ensure your credit report is accurate and up-to-date to prevent delays.

These FHA loan options provide flexible financing solutions for homebuyers looking to purchase or improve their properties, with the added security of government backing.

Understanding FHA 203k and One-Time Close Loans

FHA 203k loans, also known as rehabilitation or renovation loans, are designed for homeowners looking to make improvements to their property. These loans are insured by the Federal Housing Administration (FHA). Key features include:

High Loan-to-Value Ratio: Allows borrowers to finance a large portion of home improvement costs.

Government-Backed: Insured by the government, offering security to lenders and borrowers.

FHA One-Time Close Loans

The FHA One-Time Close Loan is a mortgage program that combines the construction, lot purchase, and permanent financing into a single loan with one closing. This loan is available for:

Benefits of the One-Time Close Loan

Single Closing: Unlike traditional construction loans that require two closings, this loan combines construction and permanent financing into one closing, simplifying the process.

No Re-qualification Needed: Borrowers do not need to re-qualify for a permanent mortgage after construction, avoiding additional credit checks, employment verification, and closing costs.

Escrow Account: An escrow account is set up to pay construction expenses, and borrowers typically do not make mortgage payments until 60 days after the final inspection.

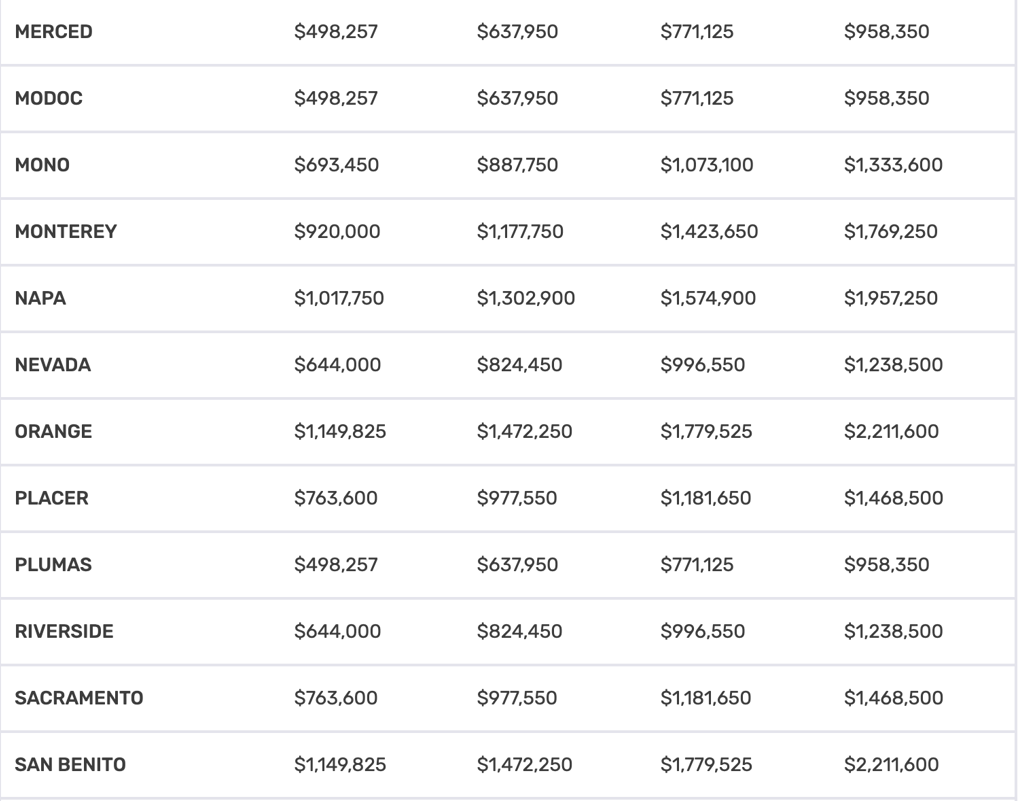

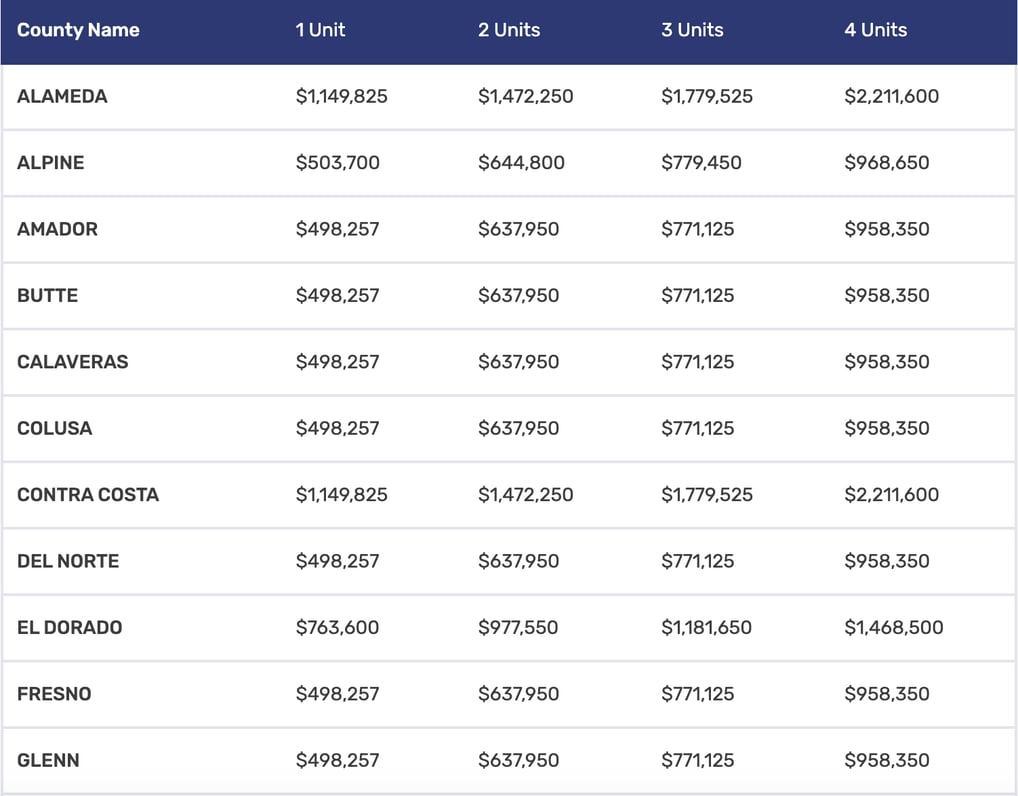

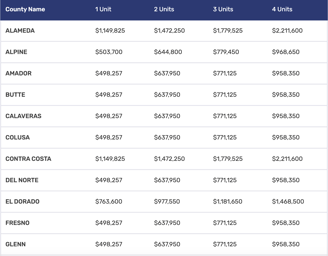

FHA mortgage lending limits in California vary based on a variety of housing types and the cost of local housing.

FHA loans are designed for borrowers who are unable to make large down payments.

2024 Lending Limits for FHA Loans in California Counties

If you have any questions about FHA loans, feel free to reach out.

I'm here to assist with the application process, eligibility requirements, and any other concerns.

Your financial well-being is my top priority, and I'm here to help you every step of the way.

Contact info:

Limited time Offer!

© 2024. All rights reserved.

OFFICE LOCATIONS:

San Francisco, CA 94118

DRE# 01814858 | NMLS # 339865

JIMMY V. NGUYEN

LOAN OFFICER | NMLS# 2502811

Take the first step towards achieving your goals and let us help you get started.

Book your FREE consultation today with NO OBLIGATION!

REALTOR | DRE# 02211200

2890 Geary Blvd. Ste. # 88

Milpitas, CA 95035

1313 N. Milpitas Blvd. Ste. #245